First in a Series

Key Takeaways

- Separate businesses may have to be treated as one employer for employee benefit plan purposes.

- Aggregation rules can affect retirement plans, health plans, COBRA, cafeteria plans, and other employee benefit arrangements.

- A retirement plan is not automatically disqualified just because another related business was overlooked, but the testing results may change significantly.

- These issues often surface when business owners have multiple entities, family ownership, related service arrangements, or leased employees.

- Business owners and advisors should disclose ownership, staffing, and related-business arrangements before plan testing or plan design decisions are made.

Employee benefit plans are not always tested one company at a time. For business owners with more than one entity, family ownership interests, related service arrangements, or workers supplied by another company, the question is often not just “Which company sponsors the plan?” but “Which employees must be counted?”

That question can affect retirement plan qualification, COBRA obligations, nondiscrimination testing, funding rules, and other benefit plan requirements. It can also surprise owners and advisors because the rules are not limited to businesses that share employees, operate in the same industry, or even do business with each other.

The Meeting That Started Innocently Enough

It was not a dark and stormy night, at least not when the meeting began.

It was a sunny afternoon, and the owners of SMALLCO, a manufacturing business, were having what was supposed to be a routine year-end review meeting with their accountant and retirement plan third party administrator, or TPA.

Then the accountant mentioned the owners’ other business, SMALL Vineyards, a small winery.

The TPA stopped.

“What winery?”

That one question changed the tone of the meeting.

As the sunny afternoon turned into a much less pleasant evening, the TPA explained that SMALLCO’s retirement plan might have a problem. If the aggregation rules applied, the winery’s employees may have had to be counted when testing SMALLCO’s retirement plan, even though those employees were not eligible to participate in the plan and may not have known the plan existed.

The TPA wondered why the business owners had not mentioned the winery. The owners wondered why the TPA had not asked better questions. The accountant said he did not think it mattered because the two businesses had nothing to do with each other.

That is exactly how these issues often arise.

The problem is not always that someone ignored a rule. Often, the problem is that no one realized the other business, ownership interest, family relationship, or staffing arrangement was relevant.

What This Series Covers

This article introduces a four-part series on the aggregation of employers and employees for employee benefit plan purposes.

In this first article, we focus on the impact of the rules and their importance.

The rest of the series explains the specific rules that may require aggregation:

- Controlled group and common control rules

- Affiliated service group rules

- Leased employee rules

- Separate line of business, or “SLOB,” rules that may permit disaggregation in limited circumstances

Impact on Retirement Plans

Why was the TPA so concerned about the winery?

Because SMALLCO’s retirement plan may have had to be tested by considering not only SMALLCO’s employees, but also the employees of SMALL Vineyards.

A tax-qualified retirement plan must satisfy various requirements under the Internal Revenue Code. Two important rules are:

- Code section 410(b), the minimum coverage requirement

- Code section 401(a)(26), the minimum participation requirement for defined benefit pension plans, including cash balance plans

These rules look at the employer’s nonexcludable employees.

That sounds simple until the aggregation rules are applied. For employee benefit plan purposes, the employer’s nonexcludable employees may include not only the common law employees of the company sponsoring the plan, but also employees of other entities that must be treated as part of the same employer group.

Aggregation Does Not Always Mean Automatic Disqualification

One common misconception is that a retirement plan is automatically disqualified if a related company’s employees were not included.

That is not always true.

A plan may still pass the applicable coverage and participation tests even if some employees who should have been considered were not actually covered. The answer depends on the demographics of the businesses involved.

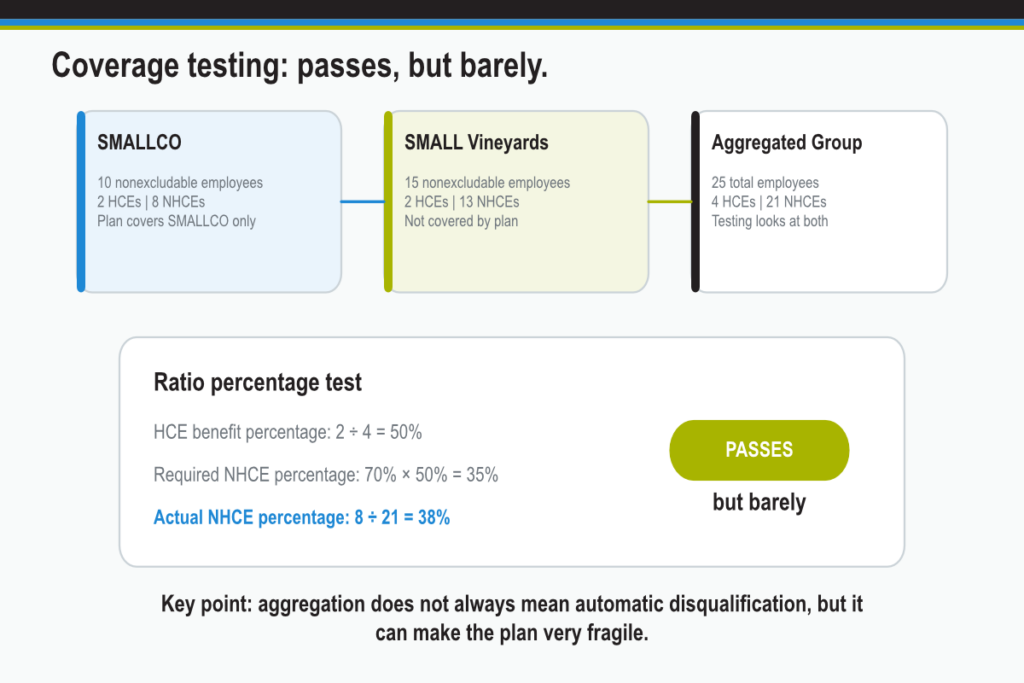

For example, assume:

- SMALLCO has 10 nonexcludable employees, 2 of whom are highly compensated employees, or HCEs.

- SMALL Vineyards has 15 nonexcludable employees, 2 of whom are HCEs.

- SMALLCO sponsors the retirement plan.

- SMALL Vineyards’ employees are not covered by the plan.

Under one of the minimum coverage tests, the ratio percentage test, SMALLCO’s plan benefits 50% of the nonexcludable HCEs in the aggregated group.

To pass this test, the plan must benefit at least 35% of the aggregated group’s nonhighly compensated employees, or NHCEs. That is 70% of the HCE benefit percentage.

In this example, SMALLCO’s plan benefits 8 of the 21 NHCEs in the aggregated group, or approximately 38%. The plan passes, but barely.

If SMALLCO had a defined benefit pension plan, it would also pass the minimum participation test because 10 of the 25 nonexcludable employees in the aggregated group benefit under the plan, or 40%.

The important point is that SMALLCO may not have a current qualification failure in this example, but it is very close. A small change in the number or category of employees could produce a very different result.

Other Retirement Plan Rules That May Be Affected

The minimum coverage and minimum participation rules may be the most obvious concerns, but they are not the only rules affected by aggregation.

The aggregation rules can also affect:

- Plan loan limits

- Nondiscrimination rules

- Annual compensation limits

- Vesting rules

- Minimum funding standards

- Excise taxes for funding deficiencies

- The definition of highly compensated employee

- Contribution and benefit limits under Code section 415

- Top-heavy plan rules

- Excise taxes on reversions

- PBGC plan termination rules

- Withdrawal liability rules

- SEP and SIMPLE IRA requirements

- Deferred compensation plan rules

In other words, aggregation is not just a technical ownership question. It can affect how a plan is designed, tested, funded, administered, and corrected.

The Opposite Problem: Aggregating When You Should Not

There is another side to the issue.

An employer that assumes related entities should be aggregated and covers all employees under one retirement plan may create a different problem if that assumption is wrong.

For example, if the plan does not include multiple employer plan provisions, and the entities are not actually treated as one employer under the aggregation rules, the plan may be operating incorrectly. Multiple employer plans are tested differently from single employer plans.

The goal is not to aggregate everyone just to be safe. The goal is to determine correctly which employers and employees must be treated together under the applicable rules.

Impact on Non-Retirement Benefit Plans

These rules are not limited to retirement plans.

Aggregation can also affect other employee benefit arrangements, including group health plans and COBRA obligations.

For example, assume SMALLCO provides a group health plan to its employees, and SMALL Vineyards provides a separate group health plan to its employees. Neither business thinks COBRA applies because each company has fewer than 20 employees.

Then SMALL Vineyards terminates an employee, Bud, who had coverage under the winery’s health plan. No COBRA notice is provided because the winery believes it is exempt as a small employer.

Later, Bud has a serious medical event and asks why COBRA coverage was never offered.

If SMALLCO and SMALL Vineyards must be aggregated, the small employer exception may not apply. The “employer” may have 25 employees, not 15. That can change the COBRA analysis entirely.

Other Welfare Benefit Rules That May Be Affected

Aggregation can also affect other non-retirement employee benefit arrangements, including:

- Group-term life insurance plans

- Self-insured medical plans

- Partially self-insured health plans with stop-loss insurance

- Medical flexible spending accounts

- The employer mandate applicable to applicable large employers

- Cafeteria plans

- Dependent care assistance programs

- Voluntary employees’ beneficiary associations, or VEBAs

- Reversions from welfare benefit funds

These rules often matter most when an employer has grown through multiple entities, family businesses, professional practices, related service companies, or ownership arrangements that were not originally designed with employee benefits in mind.

Practical Warning Signs

Aggregation should be reviewed when a business owner or advisor sees any of the following:

- One person or family owns interests in multiple businesses

- Multiple entities share owners, managers, facilities, employees, or services

- One entity provides services to another

- A professional practice is connected to a management company, lab, surgery center, imaging center, or similar service business

- A company uses workers employed by another company

- Businesses assume they are too small for certain benefit rules

- A retirement plan covers only one entity in a larger ownership structure

These facts do not automatically mean aggregation applies, but they are strong reasons to ask the question.

What to Do

If you own more than one business, advise owners who do, or work with benefit plans for companies with related ownership or staffing arrangements, the aggregation rules should be part of the conversation.

At a minimum, business owners should disclose the following to their benefits counsel, TPA, accountant, and other advisors:

- All businesses they own, directly or indirectly

- Ownership percentages

- Family ownership relationships

- Shared employees or shared services

- Management company arrangements

- Staffing, leasing, or PEO-style arrangements

- Related professional entities or service providers

- Retirement, health, cafeteria, and other employee benefit plans maintained by any related entity

The time to discover an aggregation issue is before plan testing, before a transaction, before an IRS or DOL inquiry, and before a terminated employee raises a COBRA or benefit claim.

If there is any doubt, the ownership and staffing structure should be reviewed under the applicable aggregation rules.

Read the Full Series

This article is part of a series on employee aggregation rules for benefit plans.