Third in a Series

Key Takeaways

- Businesses that are not part of a controlled group may still have to be aggregated under the affiliated service group rules.

- Affiliated service group rules often matter for professional practices, management companies, labs, surgery centers, imaging centers, and other service arrangements.

- These rules look at ownership, service relationships, and whether one organization regularly performs services for another or is associated with another in providing services.

- The analysis can be highly fact-specific, especially when services fall between regulatory safe harbors and unsafe harbors.

- Separate entities and limited ownership percentages do not necessarily avoid aggregation if the service relationship is close enough.

A controlled group analysis does not always end the aggregation inquiry. Even when the ownership percentages are not high enough to create a controlled group, businesses may still have to be aggregated if they are sufficiently connected through service relationships.

That is where the affiliated service group rules come in. These rules are especially important for professional practices and related service arrangements, including management companies, labs, surgery centers, imaging centers, office-sharing arrangements, and other structures where separate entities work together to serve clients, patients, or customers.

The issue is not simply who owns what. It is also who is performing services for whom, how the businesses are connected, and whether the structure causes employees of separate organizations to be treated as employees of one employer for employee benefit plan purposes.

Introducing Dr. D

In the first two articles in this series, we followed the owners of SMALLCO and SMALL Vineyards through the controlled group rules.

Now one of the winery owners, known here as Dr. D, has a new concern.

Dr. D owns 100% of a dental practice organized as a professional corporation. Dr. D also owns 20% of SMALL Vineyards and 50% of a dental lab.

The dental lab provides services to Dr. D’s patients, to the patients of other dentist owners of the lab, and to patients of unrelated dentists.

Dr. D’s dental corporation sponsors a retirement plan that benefits Dr. D and the practice’s small staff.

The question is whether that plan may also have to take the dental lab’s employees into account.

The good news for Dr. D is that the dental practice and dental lab may not be aggregated under the controlled group rules.

The bad news is that they may still have to be aggregated under the affiliated service group rules.

What Are the Affiliated Service Group Rules?

The affiliated service group rules are found in Code section 414(m).

They generally treat employees of each member of an affiliated service group as employed by a single employer for many employee benefit plan purposes.

There are three main affiliated service group categories:

- A-organization affiliated service groups

- B-organization affiliated service groups

- Management function affiliated service groups

The first two rules require some degree of overlapping ownership. At least one of the organizations must also be principally involved in the performance of services.

In general, an organization is less likely to be treated as a service organization if capital is a material income-producing factor. For example, a business that earns a substantial portion of its income from inventories, plant, machinery, or other equipment may not be treated the same way as a professional service organization.

The ASG rules also contain ownership attribution rules similar to the controlled group rules. For example, an owner spouse’s interest in a business may be attributed to the non-owner spouse, unless the spouses are legally separated under a decree of divorce or separate maintenance.

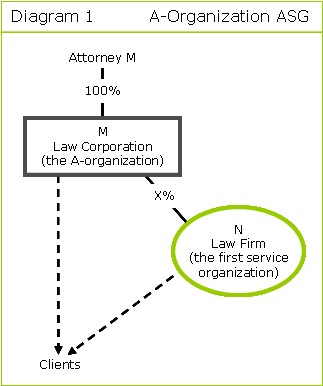

A-Organization Affiliated Service Groups

An A-organization affiliated service group generally consists of:

- A first service organization, or FSO; and

- Another service organization that is a shareholder or partner of the FSO and either regularly performs services for the FSO or is regularly associated with the FSO in performing services for third parties.

This rule often arises in professional settings.

For example, assume an attorney is incorporated and the attorney’s professional corporation is a partner in a law firm. The professional corporation and the law firm are regularly associated in performing services for clients. In that situation, the professional corporation and the law firm may be members of an A-organization affiliated service group.

Professional Service Corporations

Under proposed Treasury regulations, a corporation generally cannot be an FSO under the A-organization rule unless it is a professional service corporation.

A professional service corporation is a corporation organized under state law for the principal purpose of providing professional services and that has at least one shareholder licensed or legally authorized to render those services.

Professional services include services performed by:

- Accountants

- Actuaries

- Architects

- Attorneys

- Chiropodists

- Chiropractors

- Medical doctors

- Dentists

- Professional engineers

- Optometrists

- Osteopaths

- Podiatrists

- Psychologists

- Veterinarians

Applying the Rule to Dr. D

Dr. D’s dental corporation and the dental lab are both service organizations.

The dental lab is incorporated, but if no professional license is required for the lab’s services, it may not be a professional service corporation and may not be able to serve as the FSO under the A-organization rule.

That means the dental corporation may have to be viewed as the FSO.

The next questions are:

- Is the dental lab treated as a shareholder of Dr. D’s dental corporation through the ownership attribution rules?

- Does the dental lab regularly perform services for the dental corporation?

- Is the dental lab regularly associated with the dental corporation in performing services for third parties?

The answer may depend on the facts and circumstances.

The proposed regulations do not provide a bright-line definition of “regularly” for this purpose. One relevant factor is the income earned from the activity, but the analysis can still be uncertain.

Where this Often Comes Up

A-organization ASG issues commonly arise in professional practice structures, including:

- Physicians who own interests in surgery centers

- Physicians who own interests in imaging centers

- Dentists who own interests in dental labs

- Law firms with professional corporations as partners

- Professional practices using separate service or expense-sharing entities

- Medical or dental practices with related provider entities

These arrangements are often established for legitimate business, regulatory, operational, or investment reasons. That does not prevent the ASG rules from applying.

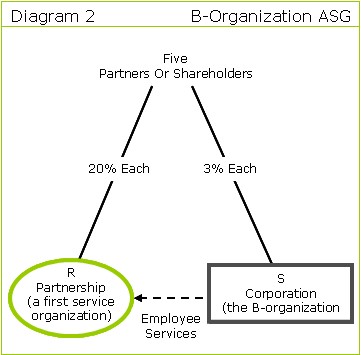

B-Organization Affiliated Service Groups

A B-organization affiliated service group generally consists of:

- An FSO; and

- Another organization, even if it is not a service organization, if a significant portion of its business is performing employee services for the FSO or an A-organization with respect to the FSO; and

- At least 10% of the interests in that organization are held by highly compensated employees of the FSO or an A-organization with respect to the FSO.

Unlike the A-organization rule, the B-organization rule can apply even if the second organization is not a service organization.

When analyzing two organizations, each organization may need to be considered as the possible FSO.

What Counts as “Significant?”

The proposed Treasury regulations provide two objective thresholds:

- If at least 10% of the potential B-organization’s total gross receipts are derived from performing services for the FSO, the services are significant.

- If less than 5% of the potential B-organization’s gross receipts from performing services are derived from performing services for the FSO, the services are not significant.

If the arrangement falls between those two thresholds, the answer depends on the facts and circumstances.

That middle ground is often where the analysis becomes difficult.

Applying the Rule to Dr. D

If the dental lab is treated as the FSO, the question becomes whether a significant portion of Dr. D’s dental corporation’s business involves performing employee services for the dental lab.

Dr. D may argue that the dental corporation is not performing services for the lab. It is performing services for patients.

There is also the ownership requirement. At least 10% of the interests in Dr. D’s dental corporation would need to be held by highly compensated employees of the dental lab. Based on the facts described, that may not be the case.

The analysis must also be reversed.

If Dr. D’s dental corporation is treated as the FSO, the question becomes whether a significant portion of the dental lab’s business involves performing employee services for the dental corporation.

Again, Dr. D may argue that the lab’s services are ultimately performed for patients, not for the dental corporation. Whether that argument succeeds may depend on the facts and the IRS’s view of the arrangement.

Management Function Affiliated Service Groups

The third ASG rule involves management organizations.

A management function affiliated service group may exist between:

- A management organization whose principal business is performing management functions on a regular and continuing basis for one recipient organization; and

- The recipient organization for which those management functions are performed.

Management functions generally refer to management activities and services historically performed by employees, including activities related to:

- Daily business operations

- Personnel

- Employee compensation and benefits

- Business planning

- Organizational structure

The withdrawn proposed regulations suggested that management activities and services could include determining, implementing, supervising, advising, or assisting with those functions.

The withdrawn proposed regulations also indicated that the principal business test could be met if more than 50% of the potential management organization’s business came from performing management functions and other services for the recipient organization.

Because some of the relevant proposed regulations were withdrawn, this area can be uncertain. The IRS and Treasury indicated that the rules may have been overly broad as applied to professionals, but comprehensive replacement guidance has not resolved every practical question.

Applying the Rule to Dr. D

In Dr. D’s case, one would not ordinarily think that the dental corporation is performing management functions for the dental lab, or that the dental lab is performing management functions for the dental corporation.

However, professional service arrangements can complicate the analysis.

If the IRS viewed one entity as performing professional or management-type services for the other, the management function ASG rule might need to be considered. The facts would matter, including how services are performed, who receives the services, and how much of the organization’s revenue is connected to the arrangement.

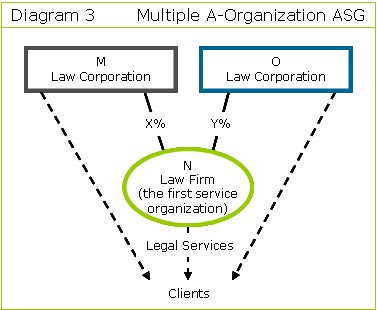

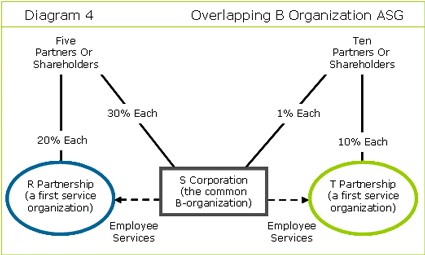

Multiple Affiliated Service Groups

The ASG analysis can become even more complicated when multiple organizations are involved.

Proposed regulations provide that multiple ASGs with a common FSO are treated as one affiliated service group consisting of the common FSO and all A-organizations and B-organizations connected to that FSO.

However, multiple ASGs are not necessarily linked together through a common A-organization or B-organization.

In practice, this means the analysis must be performed carefully across the entire ownership and service structure. It is not enough to look at only two entities in isolation if there are other related service arrangements.

Do the SLOB Rules Help?

The separate line of business rules, or SLOB rules, may provide limited relief from aggregation under the controlled group rules.

They do not provide relief from aggregation under the affiliated service group rules.

That distinction matters. A business owner may conclude that separate line of business treatment helps for controlled group purposes, but that conclusion does not end the ASG analysis.

Practical Warning Signs

An affiliated service group analysis should be considered when:

- A professional practice has owners who also own related service providers

- A management company provides services to a related business

- A lab, surgery center, imaging center, or similar entity serves professional practice owners

- Separate professional corporations participate in a larger firm or service platform

- Multiple entities are associated in serving the same clients, patients, or customers

- Employees of one organization perform services closely tied to another organization’s business

- A retirement plan covers only one entity in a broader professional or service arrangement

What to Do

Even if a controlled group analysis shows that the ownership percentages are not high enough to require aggregation, the analysis should not stop there.

Business owners and advisors should also review whether an affiliated service group exists.

That review should include:

- Ownership interests in all related service organizations

- Services performed between entities

- Services jointly performed for third parties

- Gross receipts from services between related organizations

- Professional corporation structures

- Management company arrangements

- Office-sharing or expense-sharing arrangements

- Retirement and welfare benefit plans maintained by each entity

Affiliated service group issues are fact-specific and can be easy to miss because the ownership percentages may appear too low to create a controlled group.

The key question is not only “Who owns what?”

It is also “Who is performing services for whom, and how are the businesses connected in serving clients, customers, patients, or other third parties?”

Read the Full Series

This article is part of a series on employee aggregation rules for benefit plans.