We help S and C corporation clients explore all available ESOP options. Objective guidance from a trusted advisor that fully understands the complexities of each option is imperative.

S Corporations

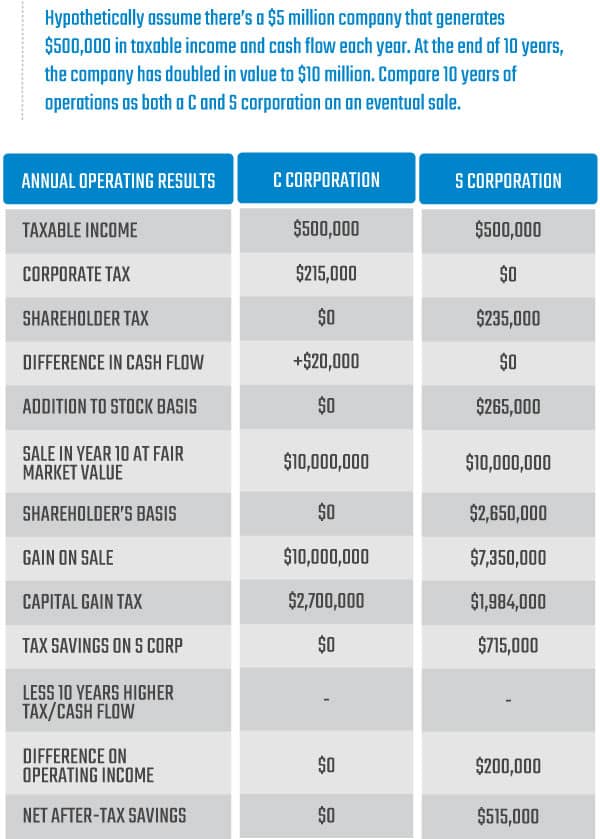

S corporation employee stock ownership plans (ESOPs) are immensely popular with our clients since they were made possible in 1998. S corporations that elected to pass through their corporate taxable income to their shareholders under Subchapter S of the Internal Revenue Code can pass through their taxable income to a tax-exempt ESOP shareholder. Combining a flow-through S corporation tax entity with the tax-exempt trust of an ESOP allows the corporate income to be tax exempt on whatever share of the S corporation is owned by the ESOP. This combined corporate and retirement plan tax structure can actually yield a 100% tax-exempt, for-profit, employee-owned company.

ESOPs, as S corporation shareholders, are also entitled to their proportionate share of any cash distributions paid by the corporation, which are invested by the ESOP as dividends and are retirement plan earnings. Well-designed S corporation ESOP transactions are able to fund between 30% and 60% of a transaction’s cost with these real tax dollars saved by the ESOP. ESOPs can also use these tax dollars saved to help fund future ESOP benefit distributions and the expenses and costs of operating the ESOP.

Put all the proclaimed incentives together and 100% of the cash flow to fund an ESOP can be saved in the ESOP or the corporation. But, these large incentives are often under-communicated and over-promoted because they have complexities, trade-offs and certain Internal Revenue Code strings attached. They require careful consideration to determine if they’re the right incentives to meet a client’s often multiple and sometimes competing objectives.

C Corporations

Most corporations, those that are called C corporations (because they are taxed under Subchapter C of the Internal Revenue Code), enjoy unique and almost legendary ESOP tax advantages that are the driving force in the growth of ESOPs since the mid- 1980s.

In very general terms, C corporation ESOPs allow:

- Selling shareholders to defer their capital gains tax on the sale of their shares to an ESOP

- Corporations to deduct up to more than twice the normal profit-sharing plan limit to fund an ESOP (50% of eligible compensation, plus interest on ESOP loans, rather than just 25%)

- Deductions for dividends paid on ESOP stock used to make payments on an ESOP loan or passed through to ESOP participants

- Departing employees to get capital gains treatment on the appreciation in their ESOP shares

In some cases, the C corporation incentives are not ideal and a transition to S corporation status is the better path. In comparison, some S corporation clients conclude that these incentives are compelling enough to revoke their subchapter S elections. It is also not unusual to take advantage of the C corporation incentives and then make the switch to S corporation status.